Thank you for helping us meet our fundraising goal!

After a year of grappling with soaring food prices, Canadians are probably dreading the big trip to the supermarket for turkey and other holiday staples. Food price inflation has slowed down in recent months, but it’s still running much hotter than the rest of the economy. Groceries are 4.7 per cent more expensive than a year ago, and slightly more than 20 per cent higher than when COVID hit.

Many Canadians instinctively blame the big supermarket chains for higher grocery prices, and that gut-level reaction is justified. Political leaders, sensing public anger, have also put the supermarkets and their executives in the hot seat. They’ve summoned grocery CEOs to repeated meetings in Ottawa, launched special studies into high food prices, and tabled various measures to take some steam out of food prices — and supermarket profits.

These include changes to competition law; a voluntary code of conduct to give smaller food suppliers better access to supermarket shelves; and a modest tax on share buybacks (which have been popular with supermarkets, and other super-profitable companies, as a way to siphon record profits to shareholders).

The federal government has even threatened an excess profits tax (similar to the ones already in place on banks and insurance companies) as leverage to nudge big supermarkets to restrain prices. The five biggest chains (Loblaw, Metro, Sobeys, Walmart and Costco, who together control over three-quarters of the market) committed to give consumers a break in the coming months. Whether that provides enough visible relief for the companies to dodge a new tax remains to be seen.

So far, none of these measures have pinched supermarkets’ profits, which continue to set records. In this regard, supermarkets are bucking the trend elsewhere in Canada’s economy, where corporate profits have moderated significantly over the past year.

Initially, many corporations profited from the pandemic. Profit-led inflation, where companies with strong market power took advantage of shortages and supply chain disruptions to jack up prices far beyond costs, afflicted many industries in 2021 and 2022.

Supermarkets were not the worst culprit. Many industries at strategic pinch-points in the overall supply chain could translate the chaos of the pandemic into the highest corporate profits in Canada’s history. That included oil and gas companies (far and away the biggest beneficiaries of post-COVID inflation), minerals and metals, building products, new cars and banks.

Total corporate profits surged 60 per cent from the end of 2019 (just before the pandemic) to the second quarter of 2022 — driving Canada’s inflation rate to over eight per cent. Unlike the “wage-price” spiral of inflation in the 1970s, post-COVID inflation was very much a “profit-price” spiral.

Since then, corporate profits have moderated: down 20 per cent over the first nine months of 2023. Normalizing profits facilitated a significant slowdown in inflation, which fell to 3.1 per cent (almost within the Bank of Canada’s target range) by October.

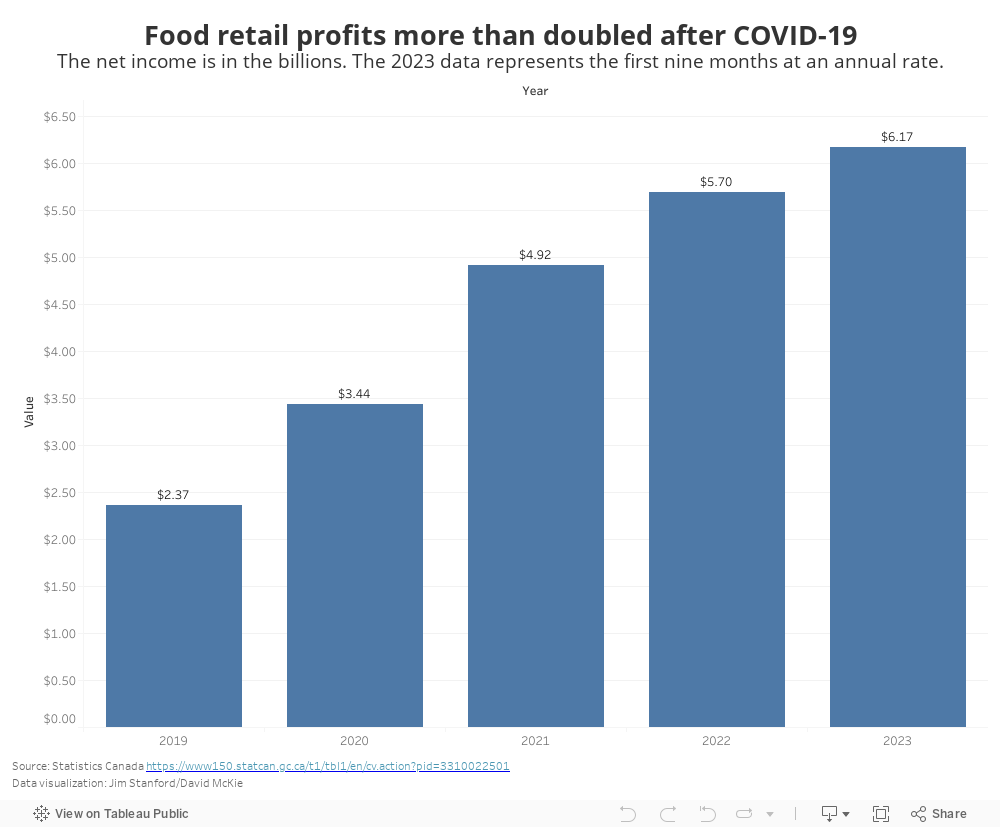

The grocery business, however, has shown no such normalization of profits, despite the repair of supply chains, falling global commodity costs, and other factors that should have produced lower prices — and lower profits. Industry-wide (including the five major chains, smaller grocers, and specialty and convenience stores), food retail profits more than doubled from typical pre-COVID levels, and they continue to set records.

Based on the first nine months of 2023, food retail profits will exceed $6 billion for the year — the highest ever.

Supermarket CEOs claim higher profits have merely been keeping up with overall costs and prices, but the hard numbers tell a different story. Measured as a proportion of total revenue in food retail, net income has more than doubled: from an average of 1.25 per cent of sales over the five years before COVID (2015-19) to more than three per cent consistently since mid-2021 (when food price inflation accelerated).

The fact that the net income margin seems “small” (three per cent is lower than typical profit margins in most industries) is often invoked to pretend that food retail is not actually very profitable. But grocery stores do not manufacture the products they sell; they simply purchase products from suppliers, add a markup, and sell them to consumers.

And while retail is an inherently “low-margin” business, this hardly means it’s not profitable. Businesses evaluate investment not according to sales margins but rather, return on invested capital. Since grocery stores are not very capital-intensive, profits relative to investment can be very high. For example, George Weston Ltd. (Loblaw’s owner) reported an annualized return on equity of 26.5 per cent over the first nine months of 2023. That’s a very high rate of profit by any standard.

Supermarkets did not start the post-COVID inflation. But they took advantage of it to capture record profits, making that inflation incrementally worse. Unless we see a quick stabilization of prices and moderation of grocery profits, we can expect food prices to remain a hot political topic right through 2024.

Jim Stanford is an economist and director of the Centre for Future Work, based in Vancouver. He recently gave testimony to the House of Commons’ Standing Committee on Agriculture and Agri-Food on the role of high retailer profits in food price inflation.

Comments

With claims like this, of "profiteering," we on the Left need to be on solid ground, such that even those with business training are forced to agree. My appreciations to you at NO then for providing real numbers and a proper bit of financial analysis, around for instance the actual net profit margins, instead of asking readers to take it on faith. Good for you to use a pre-COVID year as a baseline (as long as that year was itself typical). The more than doubling of net income, in that case, truly is eye-popping. To be really fair and beyond reproach, you might also use inflation adjusted dollars. Also, maybe adjust for the extra 2 million Canadians. Even so, your numbers definitely raise a smell. Keep up the digging. I will be re-subscribing.